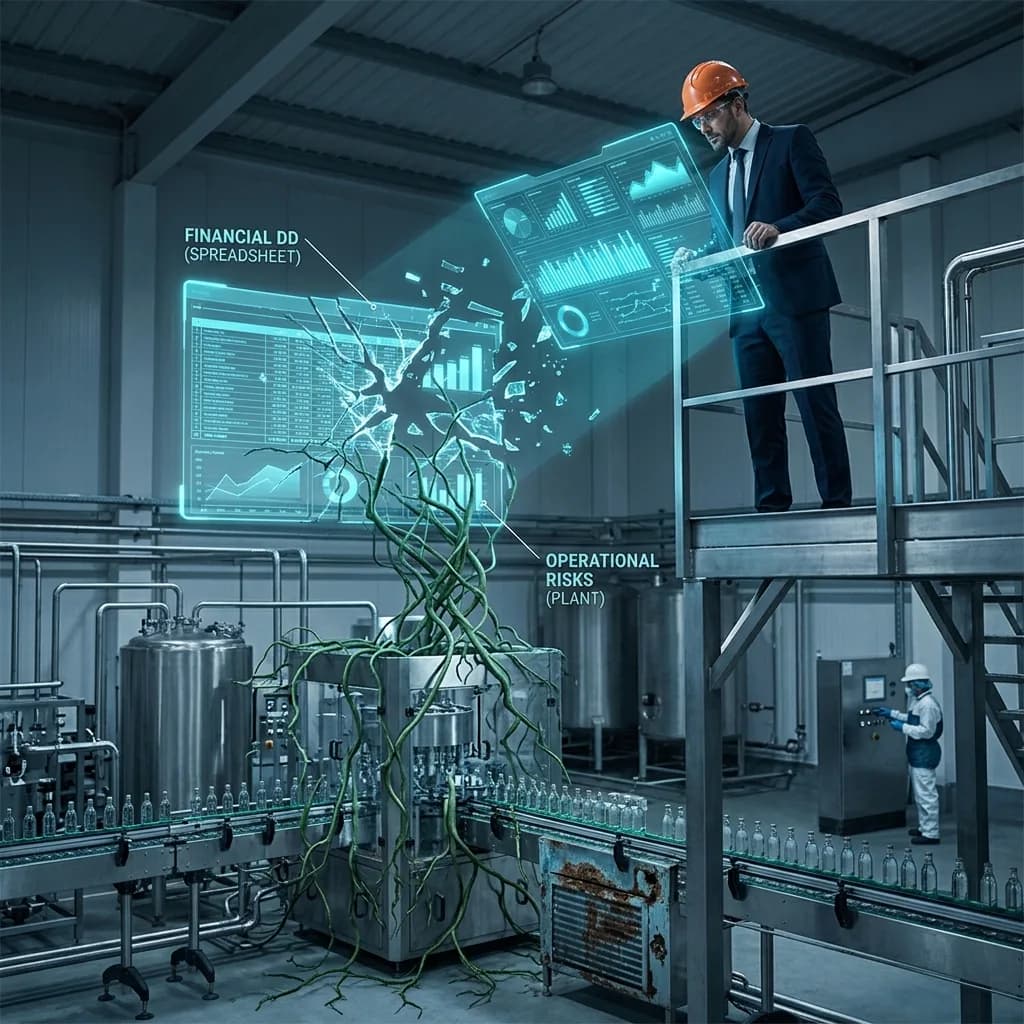

A PE fund spends $450K on financial and commercial due diligence over 10 weeks for a $90M food manufacturing acquisition. The numbers check out. The market thesis is strong. They're deep into exclusivity — and then the operational walkthrough reveals $7M in deferred maintenance, a refrigeration system at end-of-life, and capacity utilization 20 points below what management claimed.

The deal dies. The $450K is gone. And the operational issues that killed it could have been identified in the first two weeks for $40-60K.

This happens more than it should. The traditional DD sequence — financial first, commercial second, operational last — made sense when operational complexity was a secondary concern. In today's food and beverage manufacturing deals, where 7-12x EBITDA multiples leave no margin for operational surprises, that sequence is backwards.

The Sunk Cost Trap in Traditional DD Sequencing

The standard approach burns the biggest budget items early. Legal engagement, financial DD, quality of earnings — these run $200-400K before anyone sets foot in a plant. By the time operational DD begins in week 6 or 8, the fund has invested enough time and money that walking away feels painful.

This isn't just inefficient. It's structurally biased toward closing.

Every dollar spent before a material risk is identified increases the psychological pressure to rationalize that risk away. The associate who's been building the model for two months doesn't want to hear that the plant's OEE is 58%, not the 78% in the CIM. The partner who told the IC this was a strong deal doesn't want to explain why $350K of diligence produced a no-go recommendation.

The result: operational findings get minimized, purchase price adjustments get negotiated down to token amounts, and the fund closes on a deal with hidden operational risk baked in.

What Technical DD Actually Costs

Technical and operational due diligence is the lowest-cost diligence workstream — and the one most likely to uncover issues that are physically verifiable and impossible to explain away on a spreadsheet.

| Diligence Workstream | Typical Cost | Timeline |

|---|---|---|

| Financial / QofE | $150-250K | 4-8 weeks |

| Commercial / Market | $75-150K | 3-6 weeks |

| Legal | $100-200K | 6-10 weeks |

| Technical / Operational | $40-80K | 2-3 weeks |

| Environmental (Phase I/II) | $15-50K | 2-4 weeks |

The cost difference is significant. A full technical assessment runs $40-80K — a fraction of financial or legal DD — and delivers results in 2-3 weeks. More importantly, what it evaluates is physical reality. Financial statements can be managed. Capacity claims can be massaged. But a 25-year-old ammonia compressor running at 90% of its rated capacity with corroded heat exchangers is a fact that no spreadsheet can reframe.

In our experience, operational issues are among the most common reasons deals get repriced or terminated in food and beverage manufacturing. When those issues surface late, the damage is compounded — not just by the problem itself, but by the hundreds of thousands already spent getting to that point.

The Case for Leading With Technical DD

Moving technical DD to the front of the sequence — starting within days of LOI, not weeks — changes the economics and psychology of the entire process.

Lower Total Sunk Cost on Failed Deals

If a $40-60K technical assessment in weeks 1-2 identifies a deal-killing issue, the fund saves $300-400K in financial, legal, and commercial diligence that would have been wasted. Even one early kill per year saves enough to fund technical DD on every deal in the pipeline for the next several years.

Better Negotiating Position

When operational issues are found early — before the fund is emotionally and financially committed — the response is rational. Walk away, or negotiate a fair price adjustment. When those same issues are found in week 8, after $400K is spent and the IC has already given a preliminary nod, the response is to minimize and close.

A fund that identifies $4M in deferred maintenance in week 2 can renegotiate the purchase price by $4-6M (accounting for the EBITDA impact at the deal multiple). A fund that finds the same issue in week 8 typically negotiates a $500K-1M holdback and hopes for the best.

Faster Deal Velocity on Good Deals

Early technical DD doesn't just kill bad deals faster — it accelerates good ones. When the operational assessment comes back clean in week 2, the deal team proceeds with confidence. Financial DD can be scoped more efficiently because the operational thesis is already validated. The IC presentation includes real operational data instead of management estimates.

What a Front-Loaded Technical Assessment Covers

A focused technical assessment in the first two weeks of diligence doesn't replace full operational DD. It's a rapid triage designed to identify deal-killing issues before significant capital is committed.

Week 1: Desktop Review and Plant Visit (1-2 days on-site)

- Production data analysis: actual vs. claimed utilization, OEE trends, downtime patterns

- Maintenance program assessment: CMMS data, work order history, backlog quantification

- Equipment condition: age, remaining useful life, replacement cost estimates for critical systems

- Infrastructure constraints: utilities, wastewater, cold storage, loading capacity

Week 2: Report and Recommendation

- Go/no-go recommendation with supporting data

- Preliminary capex estimate for identified issues

- Risk-tiered findings: deal-killers vs. negotiation points vs. post-close value creation opportunities

- Comparison of management claims vs. observed reality

Total cost: $40-60K. Total time: 10-12 business days. The deliverable tells the fund whether to proceed with full diligence, renegotiate terms, or walk away — before another dollar is spent on financial DD.

The Counterargument — and Why It Doesn't Hold

The most common objection to leading with technical DD: "We don't want to spend money on operational assessment before we know the financial thesis works."

This sounds reasonable until you examine it. The financial thesis for a manufacturing deal is built on operational assumptions — capacity, efficiency, maintenance requirements, capex needs. Validating the financial model without validating those operational inputs is like auditing a company's revenue without checking whether the customers actually exist.

The other objection: "Sellers won't grant plant access before financial DD is underway." In practice, this is rarely true. Most sellers expect operational diligence as part of the process. The difference is timing — requesting a focused plant visit in week 1 instead of week 6. A well-structured request framed as "preliminary technical assessment" rather than "full operational DD" typically gets approved without resistance.

Rethinking the DD Sequence

The traditional sequence exists because of inertia, not logic. Financial DD goes first because it always has. But in asset-intensive industries like food manufacturing — where the physical plant is the business — starting with the asset makes more sense than starting with the spreadsheet.

The funds that consistently outperform in manufacturing deals aren't spending more on diligence. They're spending it in the right order: validate the physical asset first, confirm the financial model second, close with confidence third. When a $50K plant assessment can save $400K in wasted diligence and prevent a $15M write-down, the question isn't whether you can afford to lead with technical DD. It's whether you can afford not to.